Is it competition or cannibalisation that seals the fate of Tesco and other supermarkets?

Over the last twenty -five years the supermarkets have been rapidly expanding their presence across the country in what was often called the ‘race for space’. This included physical store building as well as banking land to prevent competitor expansion. More recently we have seen a surge in convenience store formats in town and city centres. The number of formats has tripled and food stores are now the desired anchor for many new developments and not the traditional department stores.

Added to this we have seen the rise of the discounters who until recently have been ignored and considered as not competitive or geared to a different customer demographic. How wrong can you be as the last few years have shown and that when it comes to food shopping everyone, whatever their socio-economic profile, will shop premium, mass and value and this will often be determined by the choice of stores near to them.

From 2011-14 supermarkets increased their coverage by nearly 13% whilst discounters grew by nearly 23% and of most significance has been the 54% rise of the fixed price discounters. Whilst I know that Great Britain is one of the ‘fattest’ consumer countries in Europe and has population growth this growth in physical space couple with the growth of online grocery is not sustainable and the race for space has turned into the race to the bottom. Such growth is not sustainable or wise as we enter 2015. Consumer behaviour and preferences no longer align with the ‘big shop’ once a month or indeed a week, loyalty cards no longer influence the new disloyal consumer as they once did, there for two offers are not ethical in a world where one side of the world’s food waste is on the rise whilst others starve or live on less than a $1 a day.

Change is afoot both nationally and internationally and our retail places are very much part of this sea change in attitudes and habits. Charging for plastic bags (England is the only UK country not charging a plastic bag levy) is but the thin edge of the wedge. “Around 28 million tonnes of household waste is generated in the UK every year, of which 4.9 million tonnes is packaging and 7.0 million tonnes is food waste. Carrier bags represent less than 1% of household waste but they are considered by many to be a symbol of a ‘throwaway society’ and contribute to visible litter.” (www.wrap.org.uk)

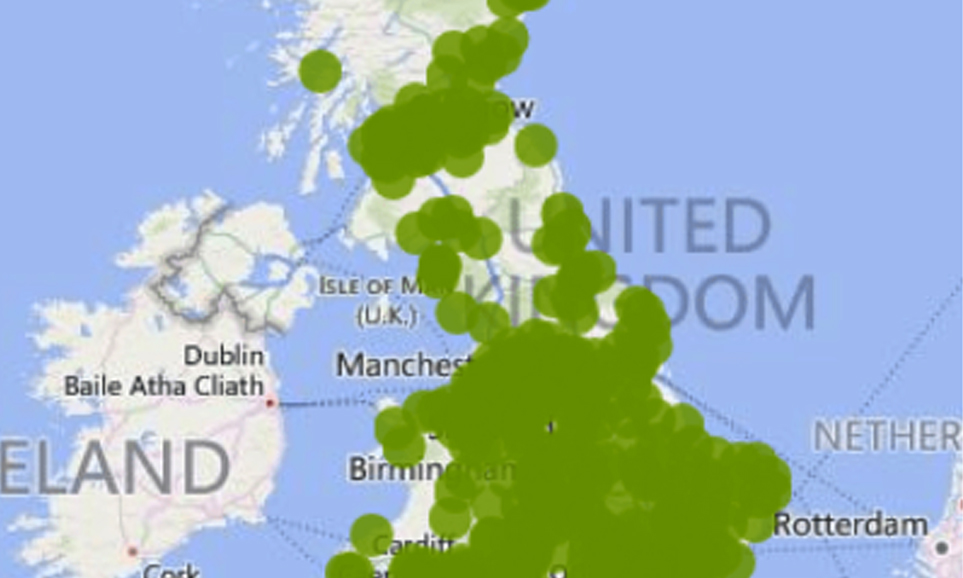

It therefore comes down to two key factors that a retailer can respond to directly – competition and/or cannibalisation. Tesco has the largest food store network in the UK and the image below from LDC’s dashboard shows this clearly (each green dot represents a Tesco supermarket) and these are just the supermarkets and not Express stores, Extras or the other fascia such as One Stop that they own.

The competition is fierce and a quick look at Norwich shows this with over 180 food stores within the postal town area and their proximity. This is illustrated by the map below and all the green dots that represent these stores. In 2012 the debate raged as to whether every UK postcode had a Tesco as claimed in a Channel 4 documentary – whilst they have in a majority the reality was not all – at that time!

The competition is fierce and a quick look at Norwich shows this with over 180 food stores within the postal town area and their proximity. This is illustrated by the map below and all the green dots that represent these stores. In 2012 the debate raged as to whether every UK postcode had a Tesco as claimed in a Channel 4 documentary – whilst they have in a majority the reality was not all – at that time!

If you then look at locations and see the concentration of a particular retailers brands/formats then it also becomes clear that cannibalisation of existing stores is an issue as you grow. Whilst technology has accelerated we are still unable to shop in two places at once – unless of course we are online! The image below shows all of the Tesco fascia around Norwich and I do not claim that there is cannibalisation for Tesco in this area it can be seen that the potential for this has increased and therefore store locations and the understanding of store catchment are key – especially as the consumer is changing so fast as are transport links and costs.

As I mentioned in a previous post the ‘big-four supermarkets will need to adapt or die’ in 2015. Insight and strategic support from The Local Data Company that can most certainly help inform and smooth such change. Know Retail. Know the Local Data Company.

Leave a comment: